PSCU, the nation’s premier payments credit union service organization, has updated its weekly transaction analysis from its Owner credit union members on a same-store basis to identify the impact of COVID-19 on consumer spending and shopping trends. An infographic can be found here.

To provide relevant updates on market performance, experts from PSCU’s Advisors Plus and Data & Analytics teams today released year-over-year weekly performance data trends. In this week’s installment, PSCU compares the 33rd week of the year (the week ending August 16, 2020 compared to the week ending August 18, 2019).

- Overall card payment volume growth rates pulled back in Week 33.

- Debit card spend was up 14.7%, which is lower than the prior four-week average of 16.6%. Transactions were up 2.4% and have been positive for seven consecutive weeks.

- Credit card spend was down 2.2% year over year, which is better than the four-week average of -3%. Transactions, hovering close to the four-week average of -6.9%, finished down 6.1%.

- Consumers continue strong usage of contactless, mobile wallets and card-not-present (CNP) alternatives, while continuing to use less cash.

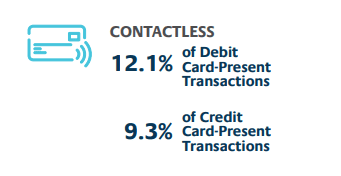

- Contactless “tap-and-go” transactions via dual interface cards continue to gain adoption. Debit contactless transactions have grown from around 8% in mid-January to 12.1% of card-present activity on contactless debit cards. Contactless credit transactions have also grown from 6.5% to 9.3% of card-present activity on contactless credit cards.

- Mobile wallet (i.e. “Pays”) transactions and purchases continue to trend up for both credit and debit cards. Debit mobile wallet purchases finished Week 33 up 74.2%. Credit mobile wallet purchases are up 52.5% year over year, in line with the prior four-week average of 48%. These results represent six supported mobile wallets: Apple Pay, Fitbit Pay, Garmin Pay, Google Pay, LG Pay and Samsung.

- We continue to see more volume conducted via Card Not Present (CNP) transactions. For credit, 51.5% of purchase volume and 41% of transactions were CNP. For debit, 41.6% of purchase volume and 28.1% of transactions were CNP. Purchase mix has held steady and is up 6.4 percentage points for credit and 6.9 for debit. Transaction mix is also steady and up 9 percentage points for credit and 7 for debit.

- Amazon, a top CNP merchant, had aggregate purchase volume increases across their various merchant categories of 80% for debit and 47% for credit.

- Cash withdrawal transactions at the ATM remain down. For the most recent week, the number of cash withdrawals was down 21.2%, just below the average for the past four weeks, which is down 20.9%.

From a merchant category perspective, trends showed mixed patterns.

- Grocery continues to perform well overall with purchases up 7.4% for debit and 14.1% for credit.

- Utilities also remain in positive territory, with purchases up 18% for debit and 6.2% for credit.

- The purchase volume of consumer goods across retail stores remains very strong, debit was up 32.2% and credit remained up 17.8% as growth continues in Electronics, Home, Discount Stores, Automobile and Sporting Goods.

- Debit spend for Restaurants stayed positive in Week 33 at 2.2%, with Fast Food Restaurants leading the way. Credit spend was down 21.2%, which is better than its four-week average of -24.4%.

- Services dipped slightly this week, with debit finishing up 10.1% and credit up 1%. Positive contributors include Healthcare, Auto, Pet and Home Services, while Personal and School Services were down.

- Some differences are evident by market, with the “hot zones” relatively in line with the overall U.S.

- Overall U.S. spend was up 14.8% for debit and down 2% for credit.

- The initial eight states/districts (CA, CT, DC, IL, LA, MI, NJ and NY) that were hardest hit by the pandemic (“hot zones”) saw debit spend up by 13.8% and for the past seven weeks have trended very close to the overall U.S. spend. Credit spend was down by 5.1% last week and has been lower than the overall U.S. spend since April by roughly four percentage points.

- The states where there were no formal “Stay At Home” orders saw a decrease in both credit and debit spend, and continue to trend under the overall U.S. For week 33, debit spend was up 6%, while the overall U.S. was up 14.8%. Credit spend is down 3.6%, compared to the overall U.S. down 2%. These states include AR, IA, ND, NE, OK, SD, UT and WY.

- PSCU’s Weekly U.S. State/Territory Analysis is available on PSCU.com/COVID19, ranking U.S. states and territories by year-over-year performance for debit purchases, credit purchases and ATM transactions.

“Card payment volumes pulled back slightly in Week 33, with merchant categories showing mixed results by sector. Compared to the strong back-to-school season in 2019, it was an overall strong week, as credit continued to improve and debit, although down from its peak, remained well above historical levels. We expect continued fluctuations as consumers establish and adjust to the ‘new normal’ while navigating ongoing uncertainty around both the pandemic and political environment.”

Glynn Frechette, SVP, Advisors Plus at PSCU

PSCU will continue to develop and share analysis of transaction trends on a regular basis.