We live in a world of almost instant gratification, seemingly without borders. You can fly across the world in less than 24 hours or order a fridge online that can be delivered to your door overnight. Why then can a cross-border payment from North America to Europe take up to 5 days?

It’s partly because, despite disruption by financial technology (fintech) companies, individuals and businesses still rely on financial institutions when moving money across borders. These institutions are not specialists in the business of cross-border payments; they provide a multitude of other financial products and services besides payment processing. Yet individuals and businesses who need to send international payments are increasingly expecting a payments process that is as simple, fast and as efficient as making domestic payments. Cross-border trade is growing rapidly as more companies source goods and services globally. The demand for user-friendly cross-border payment solutions is creating an urgent need for financial institutions to collaborate with fintech firms, some of whom are cross-border payment specialists. This article will explore what causes the payments process to be slow and inefficient, and examine the benefits of these institutions collaborating with FinTechs.

B2B wire transfers – execution remains a problem for businesses

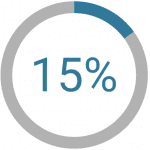

Sending and receiving payments is a multifaceted process, and the opportunity for error is everywhere. A report conducted by the School of Business at George Washington University and commissioned by Visa in 2006[1] found just 15% of all respondents reported that their payments always come with sufficient remittance information (such as customer account number and invoice number) to apply the payment correctly. Different countries have their own unique requirements for banking formats and for compliance. Different currencies may also have different conventions and formats for payments being sent – a US Dollar payment may require additional details and a different format than a local currency. Complicating matters further is that each different payment type (wire, ACH, etc.) requires specific details be provided in order to send payment. Further, to manage the risk of suspicious transaction activity, banks are required to capture information as set by government bodies and regulators. All government bodies have to be satisfied that each transaction is legitimate, and this may take time at the initiation of the transaction.

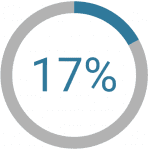

If any of the details related to a transaction are incorrect, payment can be delayed, returned or even cancelled. In such cases, manual intervention is required to correct the error, with correspondence back and forth between the various banks sending and receiving the payment. A typical business ends up researching 17% of the wire payments that it receives, at an average of $35.00 per wire and 30 minutes of time, according to the same 2006 report.[2] In addition, the impact of delayed or cancelled payments can be substantial, affecting payroll, the shipment of goods, interest charges for late payment, and hits to the financial reputation of the company. Financial institutions often bear the brunt of the blame when businesses suffer the repercussions of delays.

Power of collaboration – play to strengths rather than reinvent the wheel

Because some FinTechs specialize in cross-border payments, they have created tools that simplify the complicated payment process. Recurrent information can be loaded into a payments system to speed up processing and reduce error. For example, the rules for each country regarding banking formats and compliance requirements can be automatically applied when a transaction to that country is initiated. This eliminates the time it takes to enter information again and again, and reduces the opportunity for error during entry. Similarly, rules related to different currencies, different payments types, and so on can be entered once, and then automatically applied when a payment is initiated relevant to that set of requirements. Information related to a particular payee can also be pre-loaded, with the opportunity to change if necessary.

Rather than reinvent the wheel by trying to become cross-border specialists, financial institutions are better off leveraging a third-party fintech solution to provide clients and businesses with the easy-to-use cross-border payments solution they demand. The payoff? Satisfied customers who return to do business rather than look elsewhere for a better solution.

Moving towards faster payments – further innovation around the world in 2019

Collaborating with a FinTech can simplify the process of sending a payment across borders for businesses. But what happens once a payment is sent? Banks use any of a number of payment networks such as Automated Clearing House (ACH) or Fedwire. Funds moved through these networks may not be moved to their final destination for 2 to 5 days, and each transaction comes with a cost. Legacy systems, slow payments, and large fees have more and more businesses asking for better options.

In North America, there is currently no payment network that is low cost, widely used, and immediate. The UK, however, has the Faster Payments network, which is all three – fast, commonly used, and instantaneous. Given the negative outcomes for businesses with payments that take days to complete, there is a growing demand for speedier payment delivery.

FinTechs are constantly growing their international payment processing capabilities to cope with the needs of modern businesses. Being network agnostic allows them to build their own payment networks and embrace new technologies without the constraints of legacy systems and relationships. Financial institutions can “plug in” to these systems, gaining the benefits of speed and lower fees, without having to change their legacy systems.

In addition, all transactions are monitored through proprietary trend analytics to identify potential fraud or suspicious activities and vendor risk management is streamlined through access to a complete Due Diligence package. Beyond payment innovation, the safety and integrity of funds are the major benefits of collaboration with FinTechs, especially FinTechs with not only the technology experience but the finance experience to provide a product with a human touch.

Though FinTechs have historically been seen as competitors, many community financial institutions have begun to realize that their best strategy to remain competitive in today’s customer service landscape is often to collaborate with those FinTechs. These roles are shifting from competitor to collaborator, and the war for market share is changing to shared revenues with shared resources.

Financial Institutions are being pressured to add value to their services by offering advisory services, not just data and digital platforms. Collaborating with FinTechs can enable them to offer cutting-edge solutions while conserving resources to invest in meeting those advisory needs. It will be a challenge for community financial institutions to cut costs while maintaining strong relationships. Partnerships will allow them to do that.

As financial institutions continue to collaborate with FinTechs, businesses stand to gain from the customer-centric focus towards B2B payments and high-value wire transfers.

About Dan Caputo

Dan Caputo is the Vice President, Global Payment Solutions at AscendantFX. AscendantFX marries the world of technology and international payment delivery to provide award-winning, technology-based payment solutions for businesses. Dan can be contacted at dan.caputo@ascendantfx.com. To learn more about AscendantFX, visit www.ascendantfx.com.

[1] http://euro.ecom.cmu.edu/resources/elibrary/epay/crossborder.pdf

[2] http://euro.ecom.cmu.edu/resources/elibrary/epay/crossborder.pdf