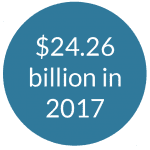

Global Card fraud losses have been escalating and seem to be growing at an alarming rate. Worldwide gross fraud losses incurred by issuers, merchants, and merchant acquirers stood at $24.26 billion in 2017, and is expected to reach $34.66 billion by 2022 – of which $12.12 billion is expected to be in the U.S., as per the Nilson Report.

With the 2018 holiday season round the corner, merchants are anticipating a 15% increase in ecommerce sales, and together with this a fraud spike. Card Fraud has been one of the major challenges for all the key players within the cards industry including merchants, issuers and merchant acquirers/ payment processors – with issuers typically absorbing 62%, and merchants bearing 38% of losses. The shortened dispute and chargeback resolution time limits mandated by VCR are difficult for merchants to adhere to, especially if they are manually reviewing these disputed transactions – merchants now have less than 30 days to draft and submit a dispute response. Merchant Acquirers, though they do not bear any direct financial implications from disputed transactions, do play the role of the entity who merchants and issuers look up to for speedy dispute and chargeback resolution. So it is important for them to resolve disputes quickly, efficiently and accurately.

So how do merchant acquirers help merchants and issuers handle fraud spikes?

Some of the larger acquirers have invested in dispute resolution technology to help merchants and issuers with quicker and faster dispute resolution.

On the flip side, most of the mid-size and small acquiring firms, that form a major chunk of the acquiring ecosystem in the country, find it impractical to invest in new and advanced dispute technologies. They typically have a team in-house dedicated to the resolution of these dispute transactions. However, during times of seasonal spikes and increased fraud spikes, these small to mid-size acquiring firms are forced to further ramp up their existing manpower to help their merchants resolve disputes within the stringent timelines. Or they fall behind in their response time. Adding additional resources means adding to fixed costs, which may not be utilized in the lean season, thus reducing overall profitability. As a result many of the merchant acquirers are now partnering with third party service providers who can manage the whole dispute resolution function.

Is Outsourcing Dispute Resolution a viable option for Merchant Acquirers?

Merchant acquirers are continuously striving to deliver a superior customer experience, faster turn times and competitive pricing to their merchants. In this current environment of heightened competition, outsourcing dispute resolution functions definitely makes sense. They should partner with service providers with experience and who have deep domain expertise in dispute resolution and related fraud. For example, being conversant with the latest categories and correct dispute reason codes helps the acquirer resolve both issuer and merchant disputes well within the stringent resolution timelines. And in addition, the acquirer can also lower their operating cost by taking advantage of the ‘pay per click’ pricing option that some of the mature service providers offer.

You can learn more about dispute resolutions here