Difficult economic times are ahead. We don’t know how difficult they’ll be, or how long they’ll last, but finance teams around the globe are bracing for them. Cash management and cost-cutting will be essential. Fraud protection—which is always a concern—will be even more important as criminals seek to capitalize on fear and confusion. If that wasn’t enough, companies have to support remote AP teams simultaneously. How can we improve payments readinesss?

By late March, a significant portion of AP staff had already begun working from home. This posed some challenges. There’s a long-held belief that anything related to the handling of company funds needs to happen inside the building. This widely accepted rule is supported by physical reality since many companies aren’t automated enough to support alternatives.

So paper invoices and expensive checks continue to send through the mail, and reference documents fill the cabinets. Even companies with cloud-based ERP systems may find them cumbersome to use when attempting to VPN in from home. AP still fields many supplier calls about payment errors or missing funds. For that, they rely on enterprise telephone systems, which are difficult to replicate in their own homes. Finally, there’s a lot of collaboration and teamwork that happens with accounts receivable, finance, and other functions, and a lot of that centers around moving paper.

Unsurprisingly, in a poll of 131 accounts payable professionals Nvoicepay conducted during a recent webcast on business continuity, 39 percent said the pandemic significantly impacted their operations. Nine percent said there was no impact because they still had to go into the office.

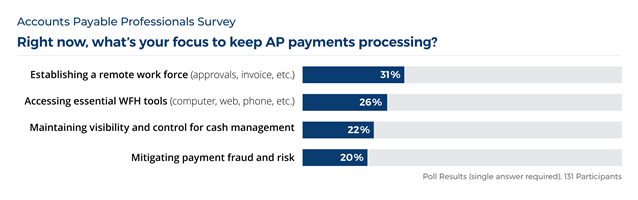

A second poll also found four key challenges accounts payable teams are working through as they implement remote payment operations:

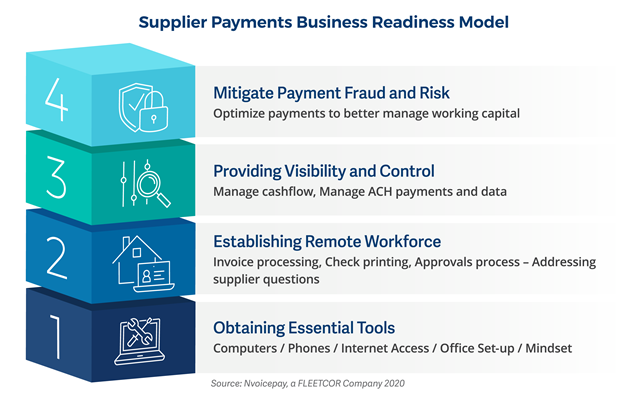

The challenge is overwhelming. Based on our experience in the market, our product team has developed a four-part hierarchy called the “Supplier Payments Readiness Model” to help customers think through all the dimensions of their remote payment organization efforts.

1. Obtaining essential tools

In our poll, 26 percent of respondents reported that equipping their teams to work from home is a top focus for payments readiness, indicating teams are still struggling with this. People will need computers. There’s a spike in demand right now, so ideally, you have some already in your inventory. If not, work on building that stock for future preparedness.

Your team will need internet access and a home office setup, preferably a secure one. They’re going to need telephones and phone routing because those trying to contact your AP team will likely call your central office phone number.

They also need collaboration tools. With employees working remotely, you may run into productivity issues if you try to have everyone work via email.

Don’t forget to address inevitable morale issues proactively. Working remotely can be lonely and stressful if you’re used to be in the office with your colleagues all the time. And, with kids schooling from home, parents are being asked to play the role of educator along with their professional role. It’s a very challenging time. Think about establishing a regular team call, as well as frequent individual check-ins.

2. Establishing remote workforce

Once you have remote capabilities set up, you’ll need to figure out your new workflow. The typical AP process has a lot of moving parts, some automated and some manual. Sketch out your whole process for payments readiness. Identify what you can currently do remotely, what can quickly become remote, and when you need people to come into the office. Designate those assignments, so you don’t have too many people showing up at once.

Start to look for technologies that can fill the gaps between manual processes, such as AP workflow systems, invoice ingestion systems, and payments automation. You may also want to make a case for a cloud-based ERP if your organization doesn’t have it, as well as e-invoicing to eliminate paper invoices. You want your team focused on cash management, not paper driving.

3. Providing visibility and control

As you redesign your workflows, re-evaluate your internal controls for payments readiness. Most established under the notion that people would be in the office, with locked filing cabinets and limited access to certain information. In a remote environment, you will probably need to put new controls in place.

Companies tend to hire more people in accounts receivable during a downturn, so there may be an uptick in inbound calls from suppliers trying to accelerate payment at the same time you’re attempting to conserve cash. Conversations between you and your suppliers need to happen so you can renegotiate terms and set them up for electronic payments. It’s best if you also work with internal business partners—such as treasury and procurement—to make sure that only prioritized payments are going out.

Maintaining internal controls will be very challenging unless you move to cloud-based technologies that give your team remote, role-based controls, visibility, and approval capabilities.

4. Mitigate payment fraud and risk

The convergence of three very challenging situations—generalized fear and chaos; hastily assembled remote work processes, and a tough economic environment—is creating a perfect storm for fraudsters to exploit. According to the 2019 AFP Payments Fraud and Control Survey Report, 80 percent of organizations surveyed said they experienced actual or attempted payment fraud in 2018. Eight percent of the respondents from that same survey said they had payment fraud losses of 0.5 to 1.5 percent of annual revenues.

This is already concerning since sophisticated cyberattacks on ACH and wire payments have been on the uptick. You want to shift vendors to electronic payments, but you also have to put new controls in place. Banks don’t provide the same positive pay or positive payee services on ACH and wire payments, and they don’t assume liability for fraud. The inability to recover those payments increases your risk. Paying your suppliers by virtual card will help you offset costs with rebates, and provide you with a more secure way to pay.

It’s anyone’s guess how long we are going to be in lockdown mode. With money tight, it’s tempting to look at these as stopgap business continuity measures that you don’t want to overinvest in. I would argue that investing in AP automation is long overdue. Even if everyone goes back to the office in a few months, do you want your employees to return to printing checks and shuffling paper? And what about the next crisis?

Forward-thinking companies have been adopting payment automation technologies precisely because they provide AP with cost savings, superior visibility and control, and fraud protection—everything that’s called for at this moment in time for payments readiness. They also allow you to maintain your operational workflow—even in a remote environment—without skipping a beat. It’s not just the right thing to do right now. It’s the right thing to do, period.